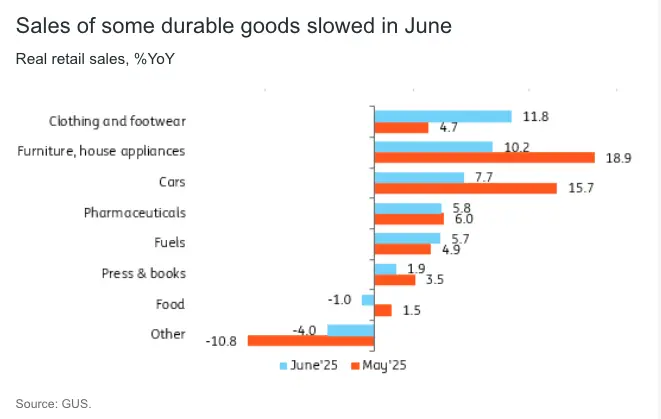

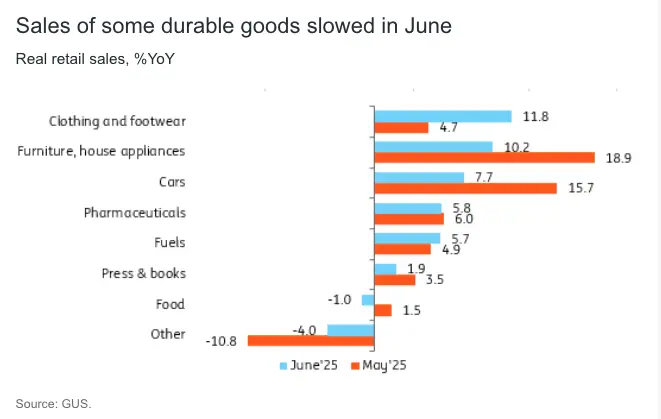

In June, the real retail sales of goods fell short of both our and market expectations, expanding by 2.2% year-on-year (ING: 4.8%; consensus: 4.1%). Substantially lower dynamics were reported in sales of vehicles and their parts (7.7% YoY vs 15.7% YoY in May) and sales of furniture, electronics and house applications (10.2% YoY vs 18.9% YoY, respectively). Food sales also declined (-1.0% YoY).

We see mixed messages from the June retail sector report. On the one hand, the annual growth of durable goods sales slowed visibly (cars, furniture, electronics, etc.) even though both current and future consumer confidence improved in June. On the other hand, solid growth was reported in the sales of fuels.

This year, June had a “long weekend” due to Corpus Christi (a non-working day in Poland), which in 2024 was celebrated in May. This could potentially translate into shifts in the structure of consumption, negatively impacting sales of goods that do not necessarily indicate weaker overall consumption. The increase in travel indicated by high fuel sales may have shifted consumer demand from goods (food and durable items) to services (accommodation and catering), which are not captured in retail sales data.

Despite weaker data for June and a slowdown in the growth of real disposable income compared to 2024, the outlook for this year’s consumption remains positive. Households have savings buffers from 2024, when the increase in spending was lower than the rise in income. Household consumption continues to be the main driver of economic growth.

We estimate that in the second quarter of this year, retail sales rose by approximately 3.5% YoY, compared to 1.6% YoY in the first quarter, partly due to the shift in Easter-related spending throughout that period relative to the previous year. We forecast that in the second quarter, growth in individual household consumption accelerated to around 4.0% YoY from 2.5% YoY in the first. As a result, GDP growth reached 3.5% YoY, compared to 3.2% YoY in the first quarter and remains on track to amount to 3.5% in 2025 as a whole. Official data on second-quarter GDP will be published on 13 August, and the detailed composition, including private consumption on 1 September.