- Strategy-wise, our Selling 5YF5Y HICPx vs US CPI trade suffered yesterday, from the US leg, while our Selling 5YF5Y FRCPIx trade grabbed a few more bp.

Risky assets, ranging from inflation forwards to equities, corrected yesterday, following the stronger-than-expected reciprocal tariffs. Regarding the US CPI profile, a lot will depend on whether these very aggressive tariffs are actually implemented, or if they are more of a cap, opening the door to negotiations.

Assuming the reciprocal tariffs are all applied with strong pass-through, we would expect US headline around 4.1-4.2% at year-end, vs our most recent forecast of around 3.3% in Tuesday’s Inflation Weekly. If there is around 50% implementation of the newly announced tariffs, we would expect headline around 3.5%; in both cases, it would be an upside revision in our forecasts. The market was pricing in around 3.7% at the Dec-25 horizon at European COB yesterday.

The impact on Eurozone inflation would be more muted, as Europe would only put tariffs on US imports (assuming full retaliation). This would be offset by weaker energy prices, slightly weaker GDP growth and possibly a redirection of international trade (namely from Asia) to Europe. In the end, it will mostly be about the balance between energy prices and retaliation.

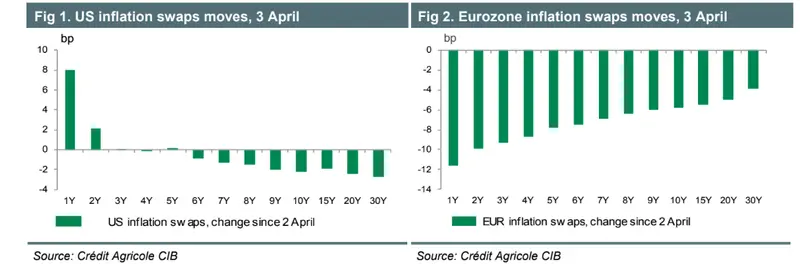

Strategy-wise, US front-end inflation swaps are about the credibility of the tariffs, while the longer end is about risk sentiment. Our Selling 5YF5Y HICPx vs US CPI trade suffered yesterday, from the US leg.

For European inflation swaps, the very front end is balanced between the risk of retaliation and energy prices (falling). The longer-end rather remains a sell in our view, considering the likely coming newsflow: international tensions, retaliations and weak growth numbers. Our Selling 5YF5Y FRCPIx trade grabbed a few more bp yesterday.

Today, the payroll data will be under scrutiny. Our house call is for NFP to rise by +135k, down modestly from +151k in January, but still a solid level given that trend job growth has likely dipped back to +100k or a bit below with immigration inflows slowing sharply.