At the time of writing, most Asian bourses were trading in the green, but S&P 500 futures were in the red. G10 FX was trading in tight ranges in Asia to start the week, with the NZD modestly outperforming and the JPY underperforming on firmer investor sentiment.

The Trump trade has been unwound, but is the USD still on (retail) sale?

The recent USD sell-off has slowed down of late, and we expect it to lose its intensity in the very near term due to the fact that: (1) the Trump trade has been largely unwound in the FX markets, with the USD having recently revisited its lows from before the US election; (2) markets have gone ahead of themselves pricing in a US recession, and we expect that the incoming US data could ease the worst of the market fears; and (3) US rates investors’ Fed outlook has become too dovish, and the outcome of the March FOMC meeting could challenge that view, in a boost to the USD.

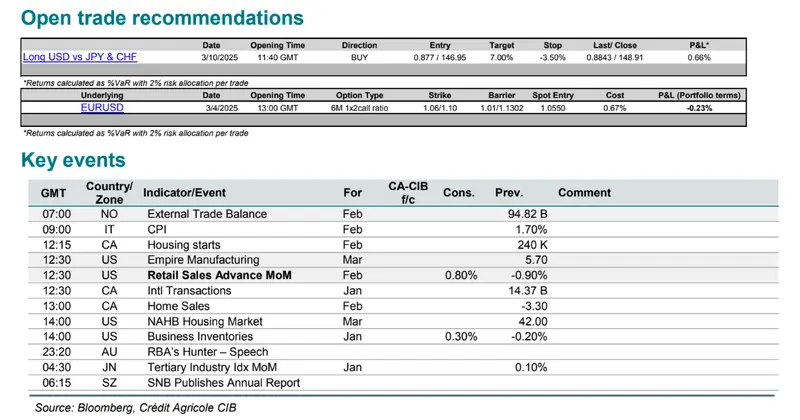

On the day, focus would be on US retail sales for February. Ahead of the release, our US economist is expecting domestic demand to rebound but by less than expected by market consensus. In particular, the headline print should come in at 0.5%MoM or below the consensus expectation of 0.7%, while retail sales ex auto & gas could disappoint as well. Turning to the FX market reaction, at the time of writing, US rates markets are pricing in 66bp of cuts by the end of 2025 – or more than the two rate cuts expected by us (and signalled by the Fed’s own December dot plot). With many Fed-related negatives already in its price, we doubt that a potential data disappointment today would trigger a resumption of the USD’s recent sell-off.

AUD: looking for a break?

AUD/USD remains stuck in its c.0.62-0.64 trading range, which has lasted for three months. The exchange rate is trapped between (1) support from improving investor sentiment towards China & China-related assets, a reluctant rate in the RBA and weakening sentiment towards the US and (2) the drag from the uncertainty generated by US President Donald Trump’s fluid tariff & foreign policies.

China’s cyclical data straddling the Lunar New Year period further buoyed sentiment by surprising to the upside today. Industrial production held up better than the consensus estimate expected and retail sales continue to grow. Housing market data showed that the sector remains in a slump, however. Later today, policymakers will provide further details on measures designed to boost the real estate and equity markets, wages & consumption as well as the birth rate. News about measures to boost Chinese consumption is usually better news for the NZD than the AUD, since NZ exports more consumer goods than Australia to China and most importantly baby milk powder.

Late this week, the RBA’s Chief Economist and Assistant Governor of Economic Group, Sarah Hunter, is expected to maintain the RBA’s reluctant rate cutter stance in her speech. The Australian rates market continues to ignore the RBA’s hawkish talk and to price in over 50bp worth of further rate cuts by the central bank. It will take data to convince investors otherwise. We also get Australian labour market data this week and weakening job advertisements and employment intentions of businesses suggest Australian employment growth will slow from the very strong growth rates of the past two months. Employment growth will likely still be strong enough to prevent a rise in the unemployment rate, however.

The FOMC meeting and US retail sales data will likely be the largest drivers of AUD/USD this week. Our US economist expects US retail sales data to bounce by more than the consensus forecasts. He expects the FOMC to be on hold and to continue suggesting it is not in a rush to cut rates further even though President Donald Trump’s trade and fiscal policies are generating higher levels of uncertainty. Both outcomes would weigh on the AUD.